")

IonQ, Inc. is at the frontier of quantum computing, using trapped-ion technology to develop highly accurate quantum systems. Since going public via a SPAC merger in 2021, IonQ has shown explosive revenue growth, expanding its industry reach and partnerships. However, profitability remains distant, and high R&D spend, insider selling, and valuation concerns cloud the short-term picture. This report offers a 360-degree analysis on IonQ’s financials, growth trajectory, order book, risks, market opportunity, valuation, and technical indicators, answering: Is IonQ a revolutionary moonshot or a risk-heavy bubble?

📈 Company Growth and Financial Performance

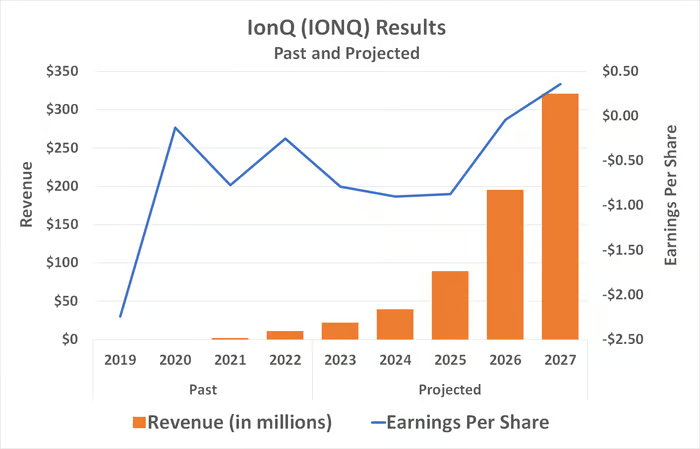

Revenue Growth Trajectory (2021–2024)

- 2021 Revenue: $2.1M

- 2022 Revenue: $11.1M (+428% YoY)

- 2023 Revenue: $22M (+98% YoY)

- 2024 Revenue: $43.1M (+95% YoY)

📌 IonQ has shown consistent exponential revenue growth, reflecting growing industry acceptance and early-stage commercial traction.

EBITDA and Profitability

| Year | EBITDA Loss | Net Loss | EPS |

|---|---|---|---|

| 2021 | -$38M | Not reported | NA |

| 2022 | -$75M | NA | NA |

| 2023 | -$126M | -$147M | -$0.69 |

| 2024 | -$213.8M | -$331.65M | -$1.56 (↓124.72% YoY) |

- Operating costs are ballooning due to cutting-edge R&D, scaling challenges, and workforce expansion.

- EPS losses have more than doubled, showing investor dilution and inefficiency in converting revenue into shareholder value.

🔍 Key Insight: IonQ is not aiming for near-term profitability; it’s building technological superiority for long-term disruption.

📦 Order Book & Business Expansion

Bookings Growth Overview

| Year | Estimated Bookings | Growth Rate |

|---|---|---|

| 2022 | ~$15M | – |

| 2023 | ~$26M | ~73% |

| 2024 | ~$40–45M | ~54–60% |

- 2024 bookings exceeded guidance ($38.5M), signaling increasing customer confidence.

- IonQ is not reliant on one sector — diversified across:

- Pharmaceuticals – molecule modeling, drug simulation

- Finance – risk optimization, complex derivative modeling

- Materials Science – simulation, nano-manufacturing

Cloud Partnerships

- Amazon Braket & Microsoft Azure Quantum allow easy global accessibility of IonQ’s systems without physical hardware purchases.

- These partnerships help IonQ scale globally without direct CAPEX-heavy deployments.

Regional Strategy

- Europe: Collaborating with EU governments under Horizon Quantum Flagship initiatives.

- Asia: Partnerships in Japan, South Korea, and India; tapping into growing national interest in quantum defense systems.

🔮 Future Projections and Strategic Roadmap

| Year | Projected Revenue | EPS Forecast |

|---|---|---|

| 2025 | $80–90M | ~ -$1.80 |

| 2026 | $130–150M | ~ -$1.00 |

| 2027+ | Break-even Possible | Positive EPS expected post-2027 |

Pipeline Catalysts

- Quantum Error Correction Algorithms (QEC) – Critical to achieving practical quantum advantage

- Partnerships with Google, Microsoft – Accelerating development and commercialization

- Government Contracts (U.S. Air Force Research Lab) – High-value institutional clients in progress

💡 IonQ is building toward a technological inflection point (Quantum Advantage). Once reached, commercial scalability will rise exponentially.

💸 Debt & Financial Health

| Metric | Value |

|---|---|

| Debt-to-Equity | Near Zero |

| Cash Reserves (2024) | ~$400M |

| 2024 Operating Cash Flow | -$150M |

- Financing via Equity Dilution: Capital raises have diluted shareholder value, a concern for long-term investors.

- Runway: With current reserves and burn rate, IonQ can operate independently for 2–3 years.

⚠ Risk: If revenue fails to meet exponential projections, another dilution round is almost certain.

🌍 Market Size & Global Opportunity

| Metric | Value |

|---|---|

| TAM U.S. (2030) | $10B |

| TAM Global (2030) | $65B |

| CAGR | ~35% |

Sector-specific Opportunity:

| Sector | Application |

|---|---|

| Pharma | Protein folding, molecule modeling |

| Finance | Algorithmic trading, credit risk modeling |

| Manufacturing | Supply chain optimization, materials discovery |

| Logistics | Route optimization, demand forecasting |

🔍 IonQ’s early presence in these sectors makes it a first-mover beneficiary, but technological readiness will decide capture rate.

📉 Market Sentiment & Influences

Recent Market Concerns:

- Stock fell from $18 to $12 in Mar 2025

- Insider selling (CEO sold $37M worth of stock) raised doubts about leadership confidence

- Tech sector outflows and currency fluctuations added volatility

Analyst Concerns:

- Overvaluation

- Earnings per share dilution

- Lack of clear near-term profitability

⚠ IonQ’s current sentiment is not bearish due to performance, but cautious due to macro and insider actions.

📊 Technical Analysis Summary (March 20, 2025)

| Metric | Value |

|---|---|

| Current Price | $12.00 |

| Support | $10.50 |

| Resistance | $15.00 |

| 50-Month MA | $13.50 |

| RSI | 40 (Near Oversold) |

Forecast:

- Short-Term (1–3 Months): Retest of $10.50, potential slide to $8

- Medium-Term (6–12 Months): Range-bound $10.50–$15

- Long-Term (1–3 Years): Breakout to $20+ possible if milestones are met

📏 Valuation Metrics

| Metric | Value | Commentary |

|---|---|---|

| Price/Sales (2024) | ~63x | Very high, but common for frontier tech |

| Price/Sales (2027 Est.) | ~43x | Still expensive vs peers |

| Price/Book | >10 | Premium vs hardware tech firms |

🧠 IonQ’s valuation is not based on earnings multiples but on optionality and future dominance in an emerging sector.

📚 Risks Overview

| Risk Type | Description |

|---|---|

| Execution Risk | Delays in reaching quantum advantage could derail projections |

| Dilution Risk | Continued equity raises hurt EPS & shareholder value |

| Market Sentiment | Insider selling + tech outflows affect price |

| Competitive Risk | IBM, Google, D-Wave are stronger financially |

| Regulatory Risk | Currently NIL, but data-security regulations may emerge |

🧠 FAQs – IonQ Investment Analysis (2025)

-

What is IonQ’s revenue growth in 2024?

- IonQ recorded $43.1 million in revenue, representing a 95% YoY growth compared to 2023.

-

Is IonQ profitable in 2025?

- No. IonQ remains unprofitable, with a net loss of $331.65 million in 2024 and projected EPS of ~ -$1.80 in 2025.

-

What industries is IonQ expanding into?

- IonQ is targeting pharmaceuticals, finance, and materials science, leveraging quantum computing for complex problem-solving.

-

Which regions is IonQ targeting for growth?

- Europe and Asia are key expansion regions, driven by government-backed quantum technology initiatives.

-

How large is IonQ’s order book in 2024?

- Estimated between $40–45 million, exceeding their $38.5M guidance.

-

Does IonQ have significant debt?

- No. IonQ has a negligible debt-to-equity ratio (~0) and is funded primarily through equity capital raises.

-

What are the key risks of investing in IonQ?

- Risks include:

- ❌ High valuation and dilution risk

- ❌ Execution delays in achieving quantum advantage

- ❌ Rising operational losses

- ❌ Insider selling affecting investor sentiment

- ❌ Competition from IBM, Google, and Rigetti

-

What is IonQ’s long-term potential?

- If IonQ achieves quantum advantage and scales commercially, it could become a dominant player in a $65B+ market by 2030.

-

Why has IonQ stock dropped recently?

- A combination of:

- CEO’s $37 million insider stock sale

- Broader tech sector correction

- Profit-taking from early investors

- Lack of near-term profitability

- A combination of:

-

What is IonQ’s future outlook?

- Short-term risks persist, but long-term growth prospects remain strong if technological milestones are met and commercial scaling succeeds.

📌 Investment Perspective

📉 Short-Term (1–3 Months)

- ⚠ Sentiment: Bearish

- 📊 Target Price Range: $10.50–$12

- 📉 Key Risks: Insider selling, market sentiment, dilution

- 🔍 Indicators: RSI ~40, below 50-MA, potential dip to $8 if support breaks

📈 Medium-Term (6–12 Months)

- ⚖ Sentiment: Neutral

- 📊 Target Price Range: $10.50–$15

- 🔄 Key Trends: Sideways consolidation unless catalyst emerges

- 🔑 Triggers: Strategic partnerships, new bookings, government contracts

🚀 Long-Term (1–3 Years)

- ✅ Sentiment: Bullish (Tech Milestone Dependent)

- 📊 Target Price Range: $18–$20+

- 💼 Drivers:

- Commercial achievement of quantum advantage

- Entry into profitable phase

- TAM growth in pharma, finance, materials, and logistics sectors

- New quantum applications and federal contracts